PPWR packaging fees are about to reshape how companies in the EU calculate packaging costs.

Most finance teams in the EU do not know this yet.

The Packaging and Packaging Waste Regulation (PPWR), Regulation (EU) 2025/40, entered into force on 11 February 2025. It applies across all EU member states from 12 August 2026. No national opt-outs. No transition grace periods for core obligations. One regulation, one standard, applied everywhere.

For CFOs and sustainability directors, this is not an environmental story. This is a cost structure story.

Let’s talk about the changes.

What PPWR does to your packaging budet?

Until now, Extended Producer Responsibility (EPR) fees varied by country and by material, but they were relatively flat within material categories. You paid a rate per kilogram of packaging placed on the market and that was mostly that.

PPWR changes this through ecomodulation.

Starting in 2025, EU member states must have eco-modulated EPR schemes in place. By July 2029, fee modulation aligned to harmonised recyclability performance grades becomes mandatory across every member state. The grades are:

Grade A: at least 95% recyclability by weight Grade B: at least 80% recyclability by weight Grade C: at least 70% recyclability by weight Below 70%: not considered recyclable at all, faces market access restrictions from 2030

Grade A packaging pays the lowest EPR fees. Packaging that scores below Grade C will face penalties, and from 2030 onward, regulatory barriers to placing it on the EU market.

Independent analysis from RegSurance projects EU EPR fees will increase by 30 to 60 percent between 2027 and 2030 across most material categories, driven by rising recycling targets, higher waste-treatment costs, and incoming carbon-based fee components. That is not a rounding error. For companies running high-volume product lines, this is a material budget exposure.

Your choice of packaging material is now a direct input into your cost model.

Where styrofoam (EPS) sits in this new reality?

Let me be direct about EPS.

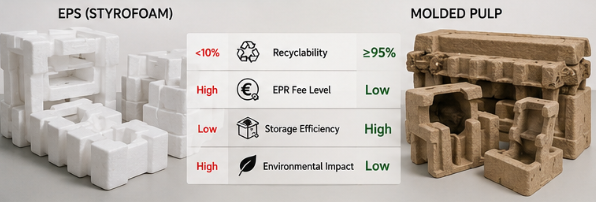

EPS (expanded polystyrene, what most people call Styrofoam) has a real-world recycling rate of less than 10 percent globally. In many EU markets, the effective recycling rate is closer to 1 to 2 percent. The infrastructure to collect and process it at scale does not exist in most of Europe.

Under PPWR’s recyclability grading system, EPS does not qualify for Grade A or B. It falls below the 70 percent threshold in most practical assessments, which means it will not be classified as recyclable under PPWR criteria. From 2030 onward, this creates both market access risk and significantly elevated EPR fee exposure.

If your product line still uses EPS as protective packaging, you are carrying a liability that compounds annually between now and 2030. And beyond the fee structure, you are carrying an ESG reporting liability that affects your credit profile with banks, your ratings with sustainability auditors, and your standing with procurement teams at large retailers who have their own sustainability targets to hit.

The question is not whether EPS becomes untenable. The question is when you want to account for that.

See how molded pulp packaging compares with EPS in recyclability, EPR fees, storage efficiency, and environmental impact.

Molded pulp packaging: the grade a case

Molded pulp packaging (also known as moulded fibre packaging, formed fibre packaging, or paper pulp packaging) is produced from recycled cellulose fibres, primarily post-consumer paper and cardboard. The end product is biodegradable, compostable, and fully accepted in existing EU paper and cardboard recycling streams.

This matters enormously under PPWR’s grading logic.

Paper and cardboard consistently achieve recyclability rates above 85 percent in European collection infrastructure. In Germany, the Netherlands, and Scandinavia, paper-based packaging routinely exceeds 90 percent. This positions uncoated molded pulp packaging solidly within Grade A criteria.

That grade difference translates directly into fee structure. Grade A packaging receives the lowest eco-modulated EPR contribution. Grade C or below receives a penalty multiplier. The gap between those two positions is not marginal. For businesses placing tens of thousands of tonnes of packaging on the EU market annually, the cumulative difference is significant across a five-year horizon.

At Tricor, we work across the full supply chain for molded pulp packaging, combining supplier access with in-house engineering and patented designs. What we see consistently in the DACH region is that companies are underestimating how fast this fee divergence will compound. The 2026 application date feels distant until it is not.

There are also secondary cost advantages worth accounting for.

Molded pulp packaging stacks and nests in ways EPS physically cannot. A common comparison in the industry: 40 molded pulp end caps occupy roughly 70 percent less warehouse space than the equivalent EPS units. That is not a sustainability talking point. That is a storage cost calculation. Fewer pallets, lower cubic meters per SKU, reduced transport frequency. For high-volume operations in the DACH region, where warehouse costs per square meter are not getting cheaper, this compounds over time.

What this means for your esg reporting

PPWR compliance and ESG performance are not separate tracks. They feed the same data.

Under CSRD (Corporate Sustainability Reporting Directive), which requires large EU companies to report on environmental impact, packaging recyclability grades and EPR fee structures are part of the documented sustainability performance. Companies that can demonstrate Grade A packaging across their product lines are documenting a measurable reduction in scope 3 emissions and waste output. This feeds directly into ESG scores used by banks for green financing, by rating agencies for sustainability assessments, and by enterprise customers doing supplier due diligence.

Companies still running EPS-heavy packaging operations will disclose that in CSRD reports. Procurement managers at major retailers read those reports.

This is the part most CFOs are not connecting yet. The packaging decision affects the balance sheet on three levels: direct EPR fees, financing conditions tied to ESG ratings, and commercial access to customers with sustainability procurement requirements.

The practical timeline you need to track

12 August 2026: PPWR applies. Packaging placed on the EU market must begin meeting core sustainability and labelling requirements.

1 January 2028: European Commission publishes formal Design for Recycling criteria. Recyclability grades become officially codified by material and design.

July 2029: Mandatory eco-modulated EPR fees aligned to harmonised recyclability grades apply across all member states.

1 January 2030: All packaging must be designed for cost-effective recycling. Packaging below Grade C faces market access restrictions.

The companies that begin transitioning packaging lines now will lock in compliance and Grade A EPR rates before the 2029 mandatory modulation. The companies that wait until 2028 will be competing for limited engineering and production capacity alongside everyone else.

In my experience, packaging engineering gets pulled into these decisions too late. The design lead time for a well-engineered molded pulp solution is not three months. It requires material testing, tooling, supply chain qualification, and often product redesign. Starting that process in 2027 because the regulation date felt far away in 2025 is a pattern I have watched play out before, in other regulatory shifts. It is expensive.

A concrete starting point

If you are a CFO or sustainability director in the DACH region and you want to understand your actual exposure, start here:

First, map your packaging by material type and weight placed on the EU market each year. This is your EPR fee base.

Second, assign a provisional recyclability grade to each packaging type based on current PPWR criteria. Anything petroleum-based, multi-layer, or with barrier coatings needs specific attention.

Third, model the fee difference between your current portfolio at projected 2029 rates and the same portfolio after substituting Grade A materials.

Fourth, factor in the logistics cost delta, particularly if you are using EPS for protective packaging in electronics, appliances, or automotive components, where nesting efficiency gains from molded pulp are most pronounced.

The numbers will tell you when it makes sense to move. In most cases, for companies with serious volume, they tell you to move now.

The one thing I want you to take away from this: PPWR is not a compliance checkbox. It is a cost structure event that will separate companies that planned for it from companies that reacted to it.

Grade A packaging pays less. Grade C pays more. The gap widens every year through 2030. Your packaging choice is now a line item decision.

What does your current packaging portfolio look like under this grading system? I would be curious to hear where others in the DACH region are in this process.

P.S. One thing I rarely see discussed: the EPR fee savings from switching to molded pulp are often more visible to the CFO than the logistics savings, because the fee shows up in a single line on the compliance report. But in high-volume operations, the storage density advantage can quietly outperform the fee reduction over a three-year period. The two are worth modelling together, not separately.

FAQ

What is PPWR and when does it apply?

PPWR stands for Packaging and Packaging Waste Regulation (EU) 2025/40. It was adopted on 19 December 2024 and entered into force on 11 February 2025. Core provisions apply from 12 August 2026 across all EU member states. It replaces the old Packaging and Packaging Waste Directive, which allowed national variation in implementation.

What is ecomodulation and how does it affect EPR fees?

Ecomodulation is the mechanism by which Extended Producer Responsibility (EPR) fees are adjusted based on a packaging’s recyclability performance. Packaging with higher recyclability grades pays lower fees. Packaging that is difficult or impossible to recycle pays higher fees or penalty multipliers. Under PPWR, harmonised ecomodulated EPR fees aligned to recyclability grades become mandatory across all EU member states from July 2029.

What recyclability grades does PPWR define?

Grade A: at least 95% recyclable by weight. Grade B: at least 80%. Grade C: at least 70%. Packaging below 70% is not considered recyclable and faces progressive market access restrictions from 2030.

Where does molded pulp packaging fall in the recyclability grading system?

Uncoated molded pulp packaging (also called moulded fibre or formed fibre packaging) is produced from paper-based cellulose fibres. It enters the existing paper and cardboard recycling stream, which achieves recycling rates above 85 percent in most EU markets. This positions standard molded pulp packaging within Grade A criteria, making it eligible for the lowest EPR fee tier.

Where does EPS (Styrofoam) fall under PPWR?

EPS has a real-world recycling rate of under 10 percent globally, and often 1 to 2 percent in EU markets where dedicated EPS collection infrastructure is absent. Under PPWR’s recyclability assessment, EPS typically falls below the 70 percent threshold, meaning it will not qualify as recyclable and will face elevated EPR fees and market access restrictions from 2030.

How much could EPR fees increase between now and 2030?

Independent analysis projects EU EPR fees will rise by 30 to 60 percent between 2027 and 2030 across most packaging material categories, driven by higher recycling targets, increased waste-treatment costs, and the introduction of carbon-based fee components. The exact increase depends on material type, member state, and recyclability grade.

Does switching to molded pulp packaging affect ESG reporting?

Yes, directly. Under CSRD, large EU companies must report on environmental impact including packaging recyclability and waste outcomes. Packaging that achieves Grade A status documents lower scope 3 waste emissions and supports stronger ESG performance scores, which feed into financing conditions, sustainability ratings, and supplier evaluations by enterprise customers.

What are the logistics advantages of molded pulp packaging compared to EPS?

Molded pulp packaging is designed to nest and stack. Industry comparisons show that 40 molded pulp end caps occupy approximately 70 percent less storage space than the equivalent EPS units. This reduces warehouse footprint, pallet frequency, and transport volume, which adds up to real cost savings in operations with high packaging throughput.

What is the lead time for transitioning from EPS to molded pulp packaging?

Transitioning requires material testing, custom tooling for moulded designs, supply chain qualification, and in some cases product or package redesign. Realistic lead times for a well-engineered solution are typically six to eighteen months depending on complexity. Companies that begin the process in 2025 or 2026 have the most flexibility. Waiting until 2027 or 2028 means competing for production capacity at the same time as the broader market.

What industries use molded pulp packaging?

Molded pulp packaging is used across electronics, consumer appliances, automotive components, food and beverage, cosmetics, and medical devices. It functions as protective packaging, end caps, trays, corner pieces, and custom-formed inserts. In any application where EPS has historically been used for cushioning or structural separation, moulded fibre is an established alternative.